Give your team a smarter way to work with product data-from attribution to insights. Harmonya connects product data to consumer reviews so you can act faster and compete smarter.

Your Shoppers Are Trading Down, Not Letting Go Of What Matters

Store brand share has hit 22%, but careful spending is not the same as indifferent spending. Here's how to identify which Demand Themes to protect in a trade-down market.

The Trade-Down Story Is Real

Private label is having a moment. Store brand dollar share across food and beverage has climbed to 22% (the fastest growth rate in years), according to Circana's 2025 private label report. Consumer surveys consistently rank price as the top purchase driver heading into 2025.

The standard read on this data is straightforward: shoppers are tightening up, and national brands are losing ground. That's true as far as it goes.

What it misses is the mechanism. Consumers aren't abandoning preferences, they're making tradeoffs. And tradeoffs require a hierarchy. Something gets protected. Something gets cut. The brands that know which is which in their category have a meaningful advantage over those operating on assumptions.

McKinsey's 2024 consumer research makes the asymmetry explicit: while 74% of consumers are trading down in some spending categories, middle-income consumers protect health and wellness spending at rates comparable to high-income consumers. Careful spending is selective spending. The categories and attributes consumers care about most continue to hold despite significant price pressure.

Not All Demand Themes Are Created Equal

Every product category contains a set of Demand Themes: structured clusters of product attributes that reflect what consumers are actually buying into when they choose one product over another. Clean ingredients. Functional benefits. Portion awareness. Indulgence. Convenience. Flavor differentiation. These themes aren't equal in how consumers value them, and that gap widens under economic pressure.

Some Demand Themes compress when wallets tighten. Others hold. A few actually strengthen.

This isn't a new phenomenon. Research on consumer behavior during prior downturns has consistently shown that attributes tied to health, efficacy, or identity retain purchase intent even as overall category spending contracts. The same pattern is playing out now, but the specific themes holding versus compressing vary significantly by category, and they don't always align with what brand teams assume.

The practical question for brand teams today isn't whether trade-down is happening. It's: which Demand Themes in my specific category are still commanding a premium, and which have quietly gone commoditized in the consumer's mind?

The Brands Getting This Wrong Are Making the Same Mistake

The default response to a trade-down environment is usually some combination of price promotion, pack size optimization, and value messaging. These are reasonable levers. They're also largely symmetric because every brand in the category can pull them, and most already are.

What gets missed in that playbook is positioning. Specifically, the risk of muting or cutting the Demand Themes that are still driving purchase intent among consumers who haven't traded out of the category entirely.

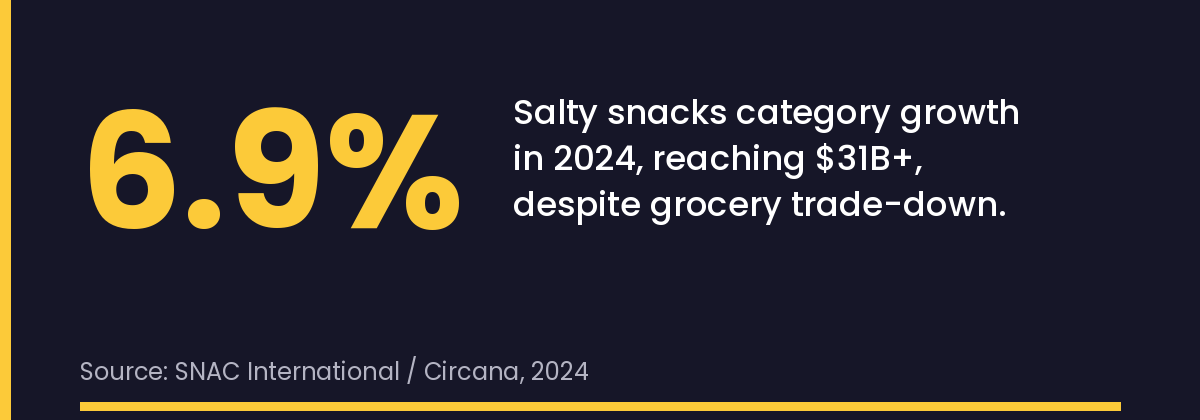

Consider salty snacks, where trade-down pressure is real but consumer engagement is not. The category grew 6.9% to over $31 billion in 2024, driven by younger consumers continuing to prioritize snacking even as overall grocery budgets tightened (SNAC International / Circana, 2024). The category is holding. But holding how, and for whom, and on which attributes...that's not visible in the headline number.

A brand managing to price and promotion alone in this environment may be eroding its association with the Demand Themes (better-for-you ingredients, clean-label credentials, specific flavor differentiation) that its most loyal buyers are still willing to pay for.

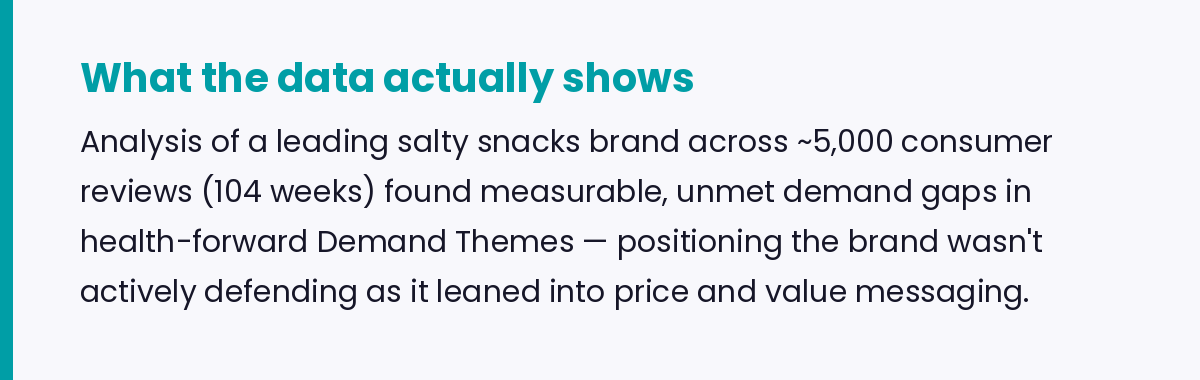

Our analysis of a leading salty snacks brand across roughly 5,000 consumer reviews spanning two years found the signal clear: health-forward positioning had measurable, unmet demand gaps the brand wasn't addressing in its product or marketing claims. The consumers who hadn't traded down were still there. The brand just hadn't maintained the attribute-level alignment that would keep them.

By the time that kind of erosion shows up in sales data, it's already happened in the consumer's mental model. Research by marketing effectiveness analysts Les Binet and Peter Field consistently shows that over-indexing on price activation at the expense of brand-building erodes long-term brand value, and rebuilding it costs substantially more than protecting it.

What It Looks Like to Know Your Demand Themes

The brands navigating this moment well aren't necessarily spending more on research. They're asking a more precise question: at the attribute level, which parts of my portfolio are outperforming the category right now, and what do those attributes have in common?

When you can attach commercial weight to specific Demand Themes (not just track share of voice or sentiment) the picture gets much clearer. SKUs indexed to certain theme clusters are outperforming the category. Others are tracking with private label, and that gap is the signal.

Harmonya's Demand Theme Framework structures product attributes and consumer language at the UPC level into standardized, enterprise-governed themes across portfolios and competitors. The Brand Scorecard benchmarks every theme, showing exactly how each brand and competitor indexes, which themes are over-represented, which are underexposed, and where the whitespace is. The result is a ranked, structured view of which Demand Themes are still driving category choice versus which consumers have effectively decided they can live without.

That distinction requires structured data at the product level. And in a market where every brand is watching the same top-line trade-down numbers, the teams with Demand Theme clarity are making better decisions about where to protect positioning and where to compete on price.

The Implication for Spring Planning

Category reviews, annual planning, and retailer sell-ins are happening now. The brands walking into those conversations with Demand Theme performance data are telling a fundamentally different story.

The argument isn't complicated: these are the themes our buyers are still choosing to pay for, here is how we compare to competitors within each one, and here is why our portfolio is positioned around them rather than away from them.

That's a story about brand strength in a difficult environment. It's also a story that's very hard to tell without a structured view of demand at the product level.

The Brands That Get Through This Intact Will Know What to Protect

Trade-down cycles end. When they do, the brands that held their positioning around the Demand Themes consumers actually care about will be in a stronger place than those that competed on price and lost the thread of what made them worth paying for.

Teams that can see which Demand Themes are still driving category outperformance, and align portfolio and marketing decisions around that structured view, will emerge from this moment with more than share. They'll emerge with a clearer picture of what their brand actually means to the people still buying it.

Teams that harmonize product data, consumer feedback, and market signals see what's shaping demand faster and with more confidence. Let's talk about how Harmonya turns fragmented data into decision-ready intelligence.

Schedule a personalized demo to see how Harmonya enriches product data, surfaces high-growth attributes, and maps shopper language back to the SKU level. We’ll walk through relevant category workflows, show how teams move from data cleanup to action, and answer questions about fit. Want proof first? Watch the Harmonya Enrichment Overview or explore Case Studies before booking.